“A Beijing-based private equity manager who bought a $2.3-million home in the hot Vancouver real estate market said he did that while earning just $19,000 a year. He also wired nearly $2-million to his family in Canada during the same period.

Jing Sun is among several foreign investors who bought property in Canada in recent years, but kept the extent of their wealth out of view of the tax authorities and the courts, a Globe and Mail investigation has found.

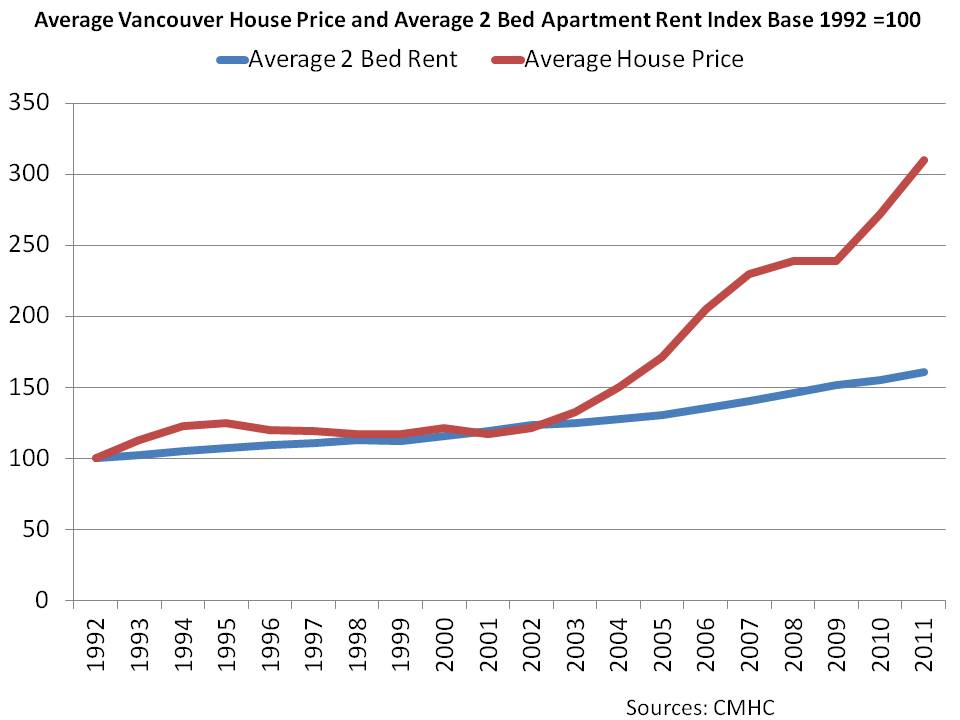

The Globe’s findings come amid a controversy in Vancouver, where many blame foreign buyers for soaring house prices that have made a single-family home unattainable for some long-time residents. The Urban Development Institute will tackle the topic for the first time in a sold-out public forum on Wednesday in Vancouver.

The subject became an election issue when Conservative Leader Stephen Harper promised to collect data on foreign ownership of Canadian real estate and to consider new taxes and regulations to keep housing affordable.

An in-depth look at public data – including land titles, tax reporting and court records – revealed a distinct pattern, suggesting the typical wealthy foreign family buying Vancouver real estate pays little or no income or capital gains tax.

“I actually have clients in this circumstance,” said David Chodikoff, a Toronto tax lawyer who was a prosecutor but now defends clients who have trouble with the Canada Revenue Agency.

He is among several experts who said most wealthy foreign buyers are not breaking the law, but simply using tax avoidance manoeuvres or loopholes in the system.

“They love to take advantage of Canadian tax law … and it is happening in other communities too,” Mr. Chodikoff said.

Many of the houses being snapped up are not huge mansions. Increasingly, they are family homes priced out of reach for locals whose taxes pay for public services, and some of whom earn more than the incomes reported by buyers such as Mr. Sun.

Court records show Mr. Sun’s wife lived without him in their pricey Vancouver home for six years while he sent her $260,000 a year from China. They paid $40,000 a year for their children to attend private school in Canada.

When the couple broke up, Mr. Sun stopped supporting the family. In his divorce case last year, he claimed he had been making $19,000 a year. The court asked for tax and other financial records, but he failed to produce any, the documents say.

He said his money was loans from friends and family in China. The judge did not believe that, saying his bank would not have approved his financing if he had no wealth of his own.

“In my view, the respondent has yet to overcome the unlikelihood … of a bank advancing him over $1-million [in a home mortgage] on the basis of a $19,000 salary,” B.C. Supreme Court Justice Emily Burke said last year.

Accountants and tax lawyers say it is common for investors from China to pay no income tax in Canada while moving their wealth to Canada through spouses and children here.

The Globe discovered one in three multimillion-dollar homes bought recently in Vancouver areas popular with foreign buyers is registered to a homemaker, student or corporation – one indicator of how the identity of the person who actually paid can be hidden.

When a spouse or child sells a property that is registered in their name, the real investor can avoid capital gains taxes – because the relative in Canada can claim it was their primary residence, therefore not an investment.

Other revealing data came from Statistics Canada, which tracks income that households report to the CRA.

In the Vancouver area of Dunbar, which realtors said is a top neighbourhood for Chinese clients, one in four of what Statscan calls “couple families” – excluding seniors – declared income of less than $35,000 in 2013. That puts them in the lowest tax bracket.

Given that the municipal property taxes on a $2-million to $3-million home are about $10,000, those reported income levels are questionable.

Land titles records on 250 houses bought in the past two years for more than $2-million in key Vancouver neighbourhoods indicate that 85 per cent of those new owners have Chinese names. There is no way to tell how many are Canadian. However, 2014 statistics from Macdonald Realty and ReMax show that 70 per cent of their clients were from mainland China.

The records list the occupations of non-corporate owners. The most frequent is “business person.” The next is “homemaker,” then “student.”

“When you sift through the information, you find that the wife [or student] has no income … there is no possible way they could afford to purchase the home,” Mr. Chodikoff said.

Several of the houses visited by The Globe appear to be unoccupied, with cobwebs at the front entrance and mail piled up.

One of the few owners who answered the door was a 25-year-old University of British Columbia science major who did not want to be identified. “My parents bought the house – for me to study here,” she said.

She is the registered owner of the $2-million home – but she said her parents live there too when they are not in China on business. “After I study, they will sell again.”

One of the more expensive homes bought last year – in Point Grey – is registered to a student who is not living there. It was bought for $4.8-million and has a stunning view of the mountains. It changed ownership three times in five years and is now empty.

The Globe found five out of 13 properties owned by students are empty and four are rented out, suggesting they were bought as investments.

A family friend picking up the mail at one house said the real owner is a business person in China who will not be in Canada for months. At another empty student-owned home, the backyard pool is filled with dirty water and garbage.

Many of the properties registered to homemakers are occupied. Several family members at those homes indicated the heads of the households are transferring wealth to Canada – because it is seen as a small, clean, inexpensive haven.

A homemaker listed as the owner of a $3.5-million house bought this year said her husband chose it “because it was good for our daughter’s [public] school to be nearby.”

She said she is staying in Vancouver – primarily so their children can get a Canadian education – while her husband travels back and forth.

She said the couple has permanent resident status in Canada, which benefits the family, but her husband earns good money in China from his food trading business.

A key question is whether foreign ownership actually is inflating the market while locals whose income tax dollars pay for roads and hospitals are squeezed out. If so, Canada would be losing affordable housing as well as much-needed provincial and federal tax revenue.

The data examined by The Globe suggest the foreign buyers have a significant, disproportionate impact on home prices.

One third of the 250 properties increased more than 50 per cent in price since 2010 – some of those more than doubled. They were also resold at least twice in that period.

The price of one property went up 40 per cent, then 123 per cent, in five years. The average single-family home in all of Vancouver increased 21 per cent in the same time period, according to the Canadian Real Estate Association.

Having trouble viewing this on mobile? Tap here.

Top ten price increases

Vancouver properties in Dunbar, Point Grey and South Granville from a sample of 250 homes purchased in the past two years for more than $2-million

The most revealing picture on tax avoidance emerged in court records from more than 200 B.C. divorces and other disputes involving real estate investors.

In several, the judges suspected or concluded significant overseas income was hidden.

Essentially, CRA rules say a non-resident who buys and sells Canadian property must pay capital gains and other taxes on earnings from those investments. If they have a primary residence and family living in Canada, they must file resident tax returns and report all of their income.

Some cases indicate that millionaires buy properties through relatives in Canada and then claim in their tax returns to be non-residents – which means they pay no Canadian taxes on their worldwide income. Others who file as residents appear to have grossly under-reported or failed to report their earnings.

Several cases involved multiple properties in the names of spouses, children, girlfriends and corporations.

The most clear-cut example of suspected tax evasion was a 2013 spousal support case against Hong Kong businessman David Ho.

The judge determined he had a net worth of $15-million to $20-million when his girlfriend, Jade Chen, came to Canada and started managing assets for him. The court concluded Mr. Ho’s annual income – from one bank account alone – was 100 times higher than the total income he reported to the CRA, which was as little as $1,254 in 2009.

The court concluded that Mr. Ho bought several properties in the Vancouver area. He put one in Ms. Chen’s name, another in his son’s, and two – worth $5-million – in the name of a corporation that had no purpose but to hold his assets in trust.

When a corporation sells property, the shareholders can simply sell the company’s shares to the new buyer, so the home stays in the company name. In that scenario, no one pays the B.C. provincial property transfer tax – $40,000 on a $2-million sale – because no change in owner name is registered. Unlike Ontario, B.C. has not closed this loophole.

Mr. Ho became a Canadian citizen years ago and signed up for B.C. health coverage. Until recently, however, he claimed on his taxes that he was a non-resident.

“[Mr. Ho’s accountant] advised Mr. Ho to break all significant ties with Canada, such as owning property and bank accounts, to ensure that Canadian tax authorities considered him to be non-resident,” B.C. Supreme Court Justice Victoria Gray said.

The accountant, Frank Sze of Richmond, said that sometimes owners don’t want their names attached to the properties.

“There are a lot of people who don’t want their names to appear in the land registry. They don’t want to be known,” Mr. Sze told The Globe and Mail. When asked why, he said, “Just because.”

Even after Mr. Ho began paying Canadian income taxes as a resident in 2011, he claimed his income was only $27,500, the court documents said.

“Many of the concerns about Mr. Ho’s evidence related to how he handled assets and how he reported them for tax and legal purposes,” said the judge, who awarded Ms. Chen a quarter of a million dollars.

In some cases, Chinese investors have said their income was from family gifts and loans, which are tax-exempt.

When millionaire Xiong Hu Li’s wife divorced him in 2013, he ignored court orders to produce financial records, including tax returns. Instead, court records say, he claimed that all the money invested in Vancouver while he was in China came from his parents.

His wife, Rong Yao, had a $6-million Vancouver home, a condo, a Porsche and an Audi registered in her name. She testified at one point she owned 16 properties in B.C., until her husband had them transferred into his mother’s name.

B.C. Supreme Court Justice Mark McEwan concluded Mr. Li “appears to have significant financial interests in China … millions of dollars … the money in Canada is of less consequence to him than revealing his assets appears to be.”

The judge called Mr. Li’s failure to account for his wealth “reprehensible” and awarded Ms. Yao spousal support, plus almost $4-million in assets.

Tax experts told The Globe and Mail Canada’s tax regime is not set up to collect from foreign millionaires who earn money overseas and have homes and family in Canada.

“I think it’s a serious issue and its a problem for the government and a problem for Canadians,” Mr. Chodikoff said.

“There could be a quite significant loss of tax revenue. More resources need to be pumped into the CRA – and more political will – so there is a desire to have stronger laws.”

The CRA indicated it is investigating the situation, but gave no specifics.

“There have been no prosecutions for tax evasion of people in Vancouver who claim to be non-resident or claim China as their primary residence,” a statement from the agency said.

“The CRA can, however, confirm that it has numerous ongoing investigations across Canada, some relating to residential real estate.”

An accountant in Vancouver who spoke on condition that he not be named said that the point is to remove the money from China.

“The picture is, basically, a lot of these people don’t really live here,” said the accountant, who came to Canada several years ago, and has wealthy Chinese clients.

“The guy in China wants to shift the money to the children – to get it out of China. Then if the Chinese government goes after the man, the assets are with the children.”

{kind=link}